50/30/20 Budget Calculator

What's the best way to divide your paycheck? The 50/30/20 Rule uses just three simple numbers to get your finances back on track.

|

With a realistic budget, you can hit your long-term financial goals and live comfortably.

But setting the budget can be difficult on its own. Especially if your income varies or you're paid irregularly.

In this article, find out how to divide your paycheck according to the 50/30/20 rule. Plus, learn what's included in your 20% savings category and when it's appropriate to adjust your budget.

What Is the 50/30/20 Rule?

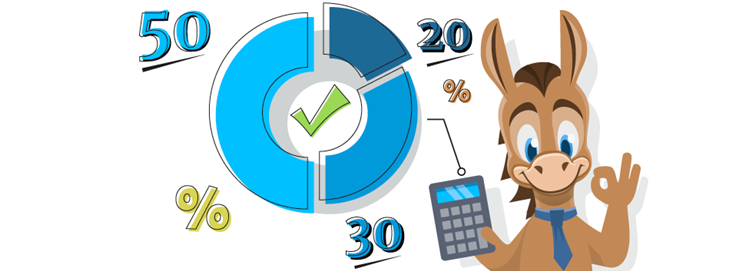

The 50/30/20 Rule is a budgeting plan introduced by Senator Elizabeth Warren. In this budgeting rule, your monthly after-tax income is split into the below categories:

- 50% is spent on "needs"

- 30% is spent on "wants"

- 20% is set aside for savings

The 50/30/20 rule is popular because it's simple, easy to remember, and easy to stick to.

Keep in mind, this is only a rule of thumb. It's okay if those percentages spill over a bit. The main goal is to get you to set aside a healthy amount for savings and to avoid overspending on wants.

50%: Your Needs

Half (or roughly half) of your monthly after-tax income is spent on absolute necessities. These are the expenses that cannot go unpaid at any given time.

This would include things like:

- Rent

- Utilities (including internet)

- Food and groceries (not including luxury meals or foods)

- Healthcare

- Transportation

- Minimum debt repayment

- Childcare

Note: While some say that internet payments fit in the "Wants" category, we'd say that internet has become an essential part of life.

As more people work from home and manage healthcare or finances online, there's reason enough to call it a necessity.

One big complaint about the 50/30/20 rule is the gray area when it comes to categorizing expenses. Something that is a 'need' to you may be a 'want' to someone else. This is completely okay. Use your best judgement to decide if something is required to keep you afloat financially, emotionally, and physically or just nice-to-have. You know yourself best.

20%: Your Savings

It may be tough to let go of 20% of your monthly take-home. We get it.

But future-you will be glad you did. Here's an example of what goes into your 20% savings category:

- Retirement account contributions

- Emergency fund contributions

- Over-minimum debt repayment

If there's one thing to take away from the 50/30/20 Rule, it's that saving is vital to your financial future. It's what enables you to retire. It can also save you and your family in the event of a job loss or expensive home repairs.

Fun Fact: The Bureau of Economic Analysis keeps tabs on how much U.S. adults are saving each month to predict consumer patterns. Check out the data to see how you stack up.

401(k) contributions are counted in the 20% savings portion because you're saving up for your future. Because these contributions are pre-tax, you may be saving more than 20% of your income. This is totally okay (and even good!). If you make monthly contributions to an IRA or Roth IRA, that would be part of the 20% savings, as well.

30%: Your Wants

Here's where the fun stuff fits in. After you budget for your needs and savings, you'll set 30% for your wants.

This includes expenses like:

- Streaming services

- TV and mobile payments

- Hobbies

- Eating at restaurants

- Gym memberships

- Personal care and grooming

- Travel and vacations

Yep, as much as we'd like to think those nightly Netflix binges are necessary for our emotional well-being, streaming services and other entertainment costs are "Wants."

If you spring for anything that's considered an "upgrade" from the most basic option (for example, groceries from a luxury market or an extensive cable TV plan), that will go in Wants, as well.

When 50/30/20 Doesn't Cut It

The 50/30/20 rule is a good framework to guide your budget. However, not everyone may find it helpful.

If you've struggled to stick with 50/30/20, consider making your own spending rule. By doing this, you can customize the rule to fit your specific needs and goals. Here's how to do it:

- First, figure out the total monthly cost of your "needs" and debt payments.

- Next, determine how much of your monthly take-home pay is spent on "wants".

- Then, create your rule. Here are some examples:

- I will set a maximum of $___ dollars to spend on "wants" per week (or per month).

- I will spend a maximum of ___% of my monthly take-home pay on "wants"

- I will aim to set aside ___% of my monthly take-home pay for savings.

- I will set a maximum of $___ dollars to spend on "wants" per week (or per month).

- Finally, make an agreement with yourself to stick to your rule (you can do it!). If you struggle, you can always make adjustments or simply try again.

Bottom Line

The 50/30/20 Rule is just one of many ways to budget, and it might not be right for everyone.

But if you question whether you're spending too much or too little on wants vs. needs, it's definitely worth checking out. You might just use it as a starting point to pinpoint the best budget for you.

If nothing else, try to save at least 20% of your monthly income. You'll be in better financial shape in the long run and your future self will thank you.

Holly Zorbas is a assistant editor at CreditDonkey, a personal finance comparison and reviews website. Write to Holly Zorbas at holly.zorbas@creditdonkey.com. Follow us on Twitter and Facebook for our latest posts.

|

|

| ||||||

|

|

|