Tips and Tricks to Save More Money

Best Jumbo CD Rates

Jumbo CDs can offer high interest for minimal risk. Find out who has the best jumbo CD rates.

Online Budgeting Tools

Looking for the best online tools to budget? See how apps like Mint, YNAB, Empower and more compare.

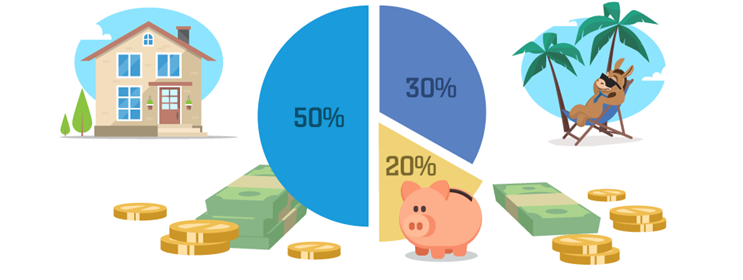

How Much Should I Save?

How much of my income should I save? Depends if it's for retirement, a house, college, a car or other goals. Find out how the 50/20/30 rule can help you.

Best Online Savings Account

Maximize your savings with the best online banks offering high-interest rates, security, and flexibility. Uncover your options.

Best High Yield Savings Accounts

Make your money work harder for you in a high-yield savings account. Here are the top savings accounts to grow your money.

Best CD Rates

Unearth the highest CD rates and maximize your savings. This list showcases the banks with the most lucrative rates.

Rankings

Online Budgeting Tools

Looking for the best online tools to budget? See how apps like Mint, YNAB, Empower and more compare.

Reviews

Acorns Review

Acorns automatically invests your spare change. But can it help make you money? Find out if this app is safe and legit.

CIT Bank Review

CIT Bank offers a high interest rate. But how reliable is this online bank? Read this review to find out if what you heard is true.

Empower Review

Empower offers wealth management services and free financial tools. But is it legit? Find out if this robo advisory service is right for you.

Recent Articles

Loan Balance Calculator

Wondering how much is left on your loan balance? Use this loan balance calculator to find out.

13 Month CD Rates

Plan ahead and grow your savings with a 13-month CD. Discover top 13-month CD rates available today.

11 Month CD Rates

Plan ahead and grow your savings with an 11-month CD. Discover top 11-month CD rates available today.

High Yield Savings Calculator

How much can your money grow in a high-yield savings account ? Use this free savings calculator to see how much you'll earn over time.

High Yield Savings Account Downside

High-yield savings accounts with good rates are tempting, but before you decide, know the downsides first. Read on for all the details.

Is High Yield Savings Account Worth It

Many high-yield savings accounts have attractive rates that are too good to pass up. But are they worth it? Read on to find out.

7 Year CD Rates

Keep your money safe and earn a fixed rate with a 7-year CD. Check out who offers the best 7-year CD rates today.

9 Month CD Rates

Lock in a high APY with a 9-month CD. Find out who has the best 9-month CD rates today.